What is Car Depreciation?

Car depreciation is the difference between a car’s value when you buy it and when you come to sell it.

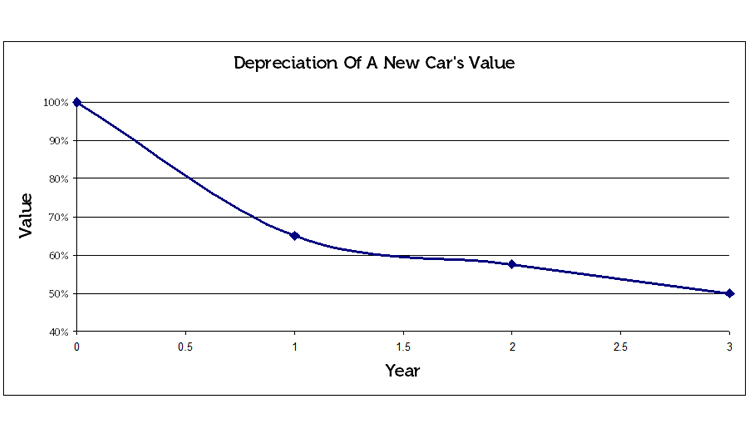

As soon as you drive your shiny new car away from the garage, it already loses around quarter of its value. Anyone who has tried to sell their new car back to the dealership can certainly vouch for this rather rapid depreciation in their car’s worth.

This drop in value varies between makes and models, but typically is between 15-35% in the first year and up to 50% or more over three years.

Consider this: You purchase a car for £20,000 and just from simply driving it off the forecourt and taking it home, it has already lost around £2,200 – £5,000. By the end of the first year it may have lost a further £2,000 and after 3 years it’s dropped by £10,000.

It sounds crazy and unimaginable why anyone would buy a brand new car but we’ll come on to that.

So why does a car’s value depreciate so quickly?

As an example, let’s look at the new car above and break this down a bit further as to where the depreciation actually comes in.

● The car costs £20,000 on the road (including all taxes and charges) as its Recommended Retail Price.

● Road tax on your car for its first 12 months is probably going to be around £150 (although it could be much more than that depending on the car’s CO2 emissions)

VAT – the Government’s contribution towards depreciation

● VAT is the big killer– and on a £20,000 car (minus the registration charges) it’s going to come in at about £4,000. That goes straight to HM Revenue and Customs. So a £20,000 new car is really just under £16,000 + tax.

● The dealership also marks up all of the prices on its cars – but we all know that. They sell vehicles from a select number of manufacturers, and the prices aren’t very competitive when comparing the same vehicle across multiple dealerships. This is because the dealers purchase the cars from the manufacturers at wholesale and that price isn’t going to vary much – you’d be looking at £1,000 to £2,000 per car.

So you as the customer might be paying £20,000 for the car, but the dealership may have bought that car for as little as £12,000. And if that’s what they are paying for a brand new car, it doesn’t bode well for how much they will pay for your used car – even if it’s virtually new. Even a day old, which is crazy but true!

Also, a customer who can buy a brand new car for £20,000 is unlikely to pay a similar amount for a used car – regardless of why it’s used. So what was a £20,000 brand new car would probably be offered for sale at £16-17,000 if it was used but ‘as new’. Take out the dealer’s costs and profit, and you’re probably back to about £12,000 again in terms of what they would buy it from you for.

Depreciation averages out over time.

The good news though (if you’re sitting there reading this peeved because you recently bought a brand new car) is that if you do intend to the keep the car for over 3 years, there’s no need to be concerned because the depreciation does average out over 3+ years.

Also keep in mind that when you buy a used car, you might not have to worry about VAT, but you will still have to factor in the dealership’s cost of sales and profits – and the costs to prepare a used car for sale may well be a lot higher than for a new car.

You really need to do your research when it comes to buying a new or used car and it does depend on the car, how much you’ll be using it and how long you think you’ll be keeping it for.

Tips for minimising car depreciation:

1. Keep the mileage down

2. Look after your car and repair any damage as soon as possible

3. Buy a nearly-new or used car to avoid the steepest depreciation

4. Avoid ‘boy racer’ modifications such as spoilers, wide wheels and flared wheel arches or any other wacky colour or print modifications

5. Sell at the right time of year – for example, convertibles in the summer and 4×4’s in the winter

6. Stick to popular colours – an outrageous shade might appeal to you, but will put off many buyers when you want to sell your car

7. Consider leasing rather than owning – then there’s no worry about the car’s depreciation, which will be built into your monthly payments

8. Do your research before buying a car – see how much values have gone down on older models and similar vehicles from the same manufacturer

9. Choose the right options when you buy – for example, metallic paint and leather are best on executive cars, while built-in sat nav and air con are desirable on mainstream cars

10. Maintain your car well – a full service history gives potential buyers peace of mind. So remember to keep all your car documents including service records and receipts safe and in one place

11. Sell your car well before its replacement model arrives in the showrooms

If you have any questions around this, please don’t hesitate to give us a shout as we are happy to give you some free advice!

Thanks

Jack